Poor interest rates, bad service and high fees push Australians to switch their Main Financial Institution in 2024

New financial data from Roy Morgan’s Single Source Program shows that Macquarie and the newer digital banks (ANZ Plus, ME Bank, Ubank and Up) have been the main beneficiaries of Main Financial Institution (MFI) switching in last 12 months.

About 667,000 Australians (2.9%) have switched their Main Financial Institution (MFI) in the last year. These customers may not have cancelled accounts or opened new accounts – but they have changed the bank they consider their Main Financial Institution (MFI).

Macquarie gained 48,000 customers and lost only 5,000 customers who consider them as their Main Financial Institution (MFI), for a net gain of 43,000, while the newer digital banks (ANZ Plus, ME Bank, Ubank and Up) gained 60,000 and lost 29,000, for a net gain of 31,000.

The big four banks and ING saw little change, with gains and losses about equal. Regional banks lost an estimated 21,000 MFI customers through switching (gaining 79,000, while losing 100,000).

Chart 1: Main Financial Institution (MFI) switched to/ switched out from (‘000s)

Source: Roy Morgan Single Source Australia, Jan. 2024 – Dec. 2024, n = 61,820.

Base: MFI switchers 14+ who provide current MFI and Switched MFI in the L12M. *Larger Regionals Banks defined as either Bendigo, BoQ, Suncorp, St George, Bank of Melbourne, BankWest, BankSA. **Newer Digital Banks defined as either ANZ Plus, ME Bank, Ubank or Up. ***Net position may not exactly equal gains minus losses due to rounding.

Reasons for switching most frequently related to rates, service and fees and charges

The top reasons for switching their Main Financial Institution in 2024 are poor interest rates, bad service, and high fees and charges.

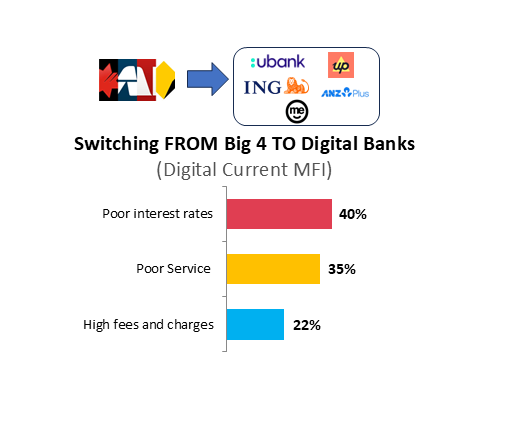

For example, among those switching from a big four bank to a digital bank, the main reason given for switching MFI is “poor interest rates”, mentioned by 40%, followed by “poor service” (35%) and “high fees and charges” (22%). The relative importance of each of these three factors varies depending on where people are switching from, and where they are switching to.

Chart 2: Reasons for switching from big four banks to digital banks

Source: Roy Morgan Single Source Australia, Jan. 2024 – Dec. 2024.

Base: MFI switchers 14+ who provide current MFI and Switched MFI in the L12M

Roy Morgan General Manager of Financial Services Suela Qemal commented:

“Australians are primarily switching their Main Financial Institution (MFI) due to poor interest rates, poor service, and high fees. The significance of each factor varies based on the bank people are leaving and the one they are moving to.

“Among those switching their MFI from a big four bank to a digital bank, 40% cite poor interest rates as the main reason, followed by 35% who point to poor service, and 22% who mention high fees. Digital banks are benefiting from offering better interest rates, which is particularly appealing during the ongoing cost-of-living crisis.

“In 2024, digital banks gained ground by attracting customers with their deposit products but are now shifting focus to mortgages. This trend is expected to grow in 2025, especially with younger customers seeking better financial solutions.”

These latest banking MFI (Main Financial Institution) estimates come from the Roy Morgan Single Source survey, derived from in-depth interviews with over 60,000 Australians each year.

Related research findings

For further in-depth analysis, view the various Banking and Finance Currency Reports.

For comments or more information about Roy Morgan Small Business Research data please contact:

Roy Morgan Enquiries

Office: +61 (3) 9224 5309

askroymorgan@roymorgan.com

About Roy Morgan

Roy Morgan is Australia’s largest independent Australian research company, with offices in each state, as well as in the U.S. and U.K. A full-service research organisation, Roy Morgan has over 80 years’ experience collecting objective, independent information on consumers.

Margin of Error

The margin of error to be allowed for in any estimate depends mainly on the number of interviews on which it is based. Margin of error gives indications of the likely range within which estimates would be 95% likely to fall, expressed as the number of percentage points above or below the actual estimate. Allowance for design effects (such as stratification and weighting) should be made as appropriate.

| Sample Size | Percentage Estimate |

| 40% – 60% | 25% or 75% | 10% or 90% | 5% or 95% | |

| 1,000 | ±3.0 | ±2.7 | ±1.9 | ±1.3 |

| 5,000 | ±1.4 | ±1.2 | ±0.8 | ±0.6 |

| 7,500 | ±1.1 | ±1.0 | ±0.7 | ±0.5 |

| 10,000 | ±1.0 | ±0.9 | ±0.6 | ±0.4 |

| 20,000 | ±0.7 | ±0.6 | ±0.4 | ±0.3 |

| 50,000 | ±0.4 | ±0.4 | ±0.3 | ±0.2 |